If you’ve recently been told you need an SR-22 in Texas, you’re probably feeling a mix of confusion and dread. The name alone sounds ominous, and a quick Google search doesn’t exactly calm the nerves. But here’s the thing: SR-22 insurance is not as complicated as it sounds, and finding affordable coverage is absolutely possible if you know what you’re dealing with.

This guide breaks down everything you need to know about SR-22 insurance in Texas in 2026 — what it is, what it costs, who offers the cheapest rates, and how to get out from under it as quickly as possible.

What Is SR-22 Insurance in Texas?

Let’s get one thing straight right away: an SR-22 is not actually an insurance policy. It’s a certificate of financial responsibility — a document your insurance company files with the Texas Department of Public Safety (DPS) on your behalf. It essentially tells the state, “Yes, this driver carries at least the minimum required coverage.”

The confusion comes from the way people talk about it. Saying “I need SR-22 insurance” is technically a shorthand. What you actually need is a standard auto insurance policy that includes an SR-22 filing attached to it.

That said, the SR-22 requirement does affect your insurance costs — sometimes significantly — because it signals to insurers that you’ve been flagged as a higher-risk driver. We’ll get into the numbers shortly.

Who Needs an SR-22 in Texas?

The Texas DPS requires an SR-22 filing in several situations. You might be required to get one if you were caught driving without insurance, if you had your license suspended or revoked, or if you were convicted of a DWI or DUI. Reckless driving convictions, multiple traffic violations in a short period, and at-fault accidents while uninsured can also trigger the requirement.

In some cases, a judge will order it as part of a court ruling. Either way, the Texas DPS will notify you directly if an SR-22 is required to reinstate or maintain your driving privileges.

If you’re not sure whether you fall into this category, it’s worth reviewing the state’s minimum car insurance requirements in Texas — understanding the baseline coverage standards makes the SR-22 requirement much easier to put in context. [Internal link: Minimum Car Insurance Requirements in Texas (2026 Update)]

How Long Do You Need SR-22 Insurance in Texas?

In most cases, Texas requires drivers to maintain SR-22 filing for two years. However, the timeframe can vary depending on the offense. More serious violations — like a DWI conviction or a second offense within a short period — may extend the requirement to as long as three years.

The clock generally starts from the date your license is reinstated, not from the date of the incident itself. That’s an important distinction. If there’s any gap in your coverage during this period, your insurer is required to notify the state, and your license could be suspended all over again — forcing you to restart the clock.

This is why it’s critical to choose a policy you can actually afford and maintain consistently. Letting it lapse is not worth the risk.

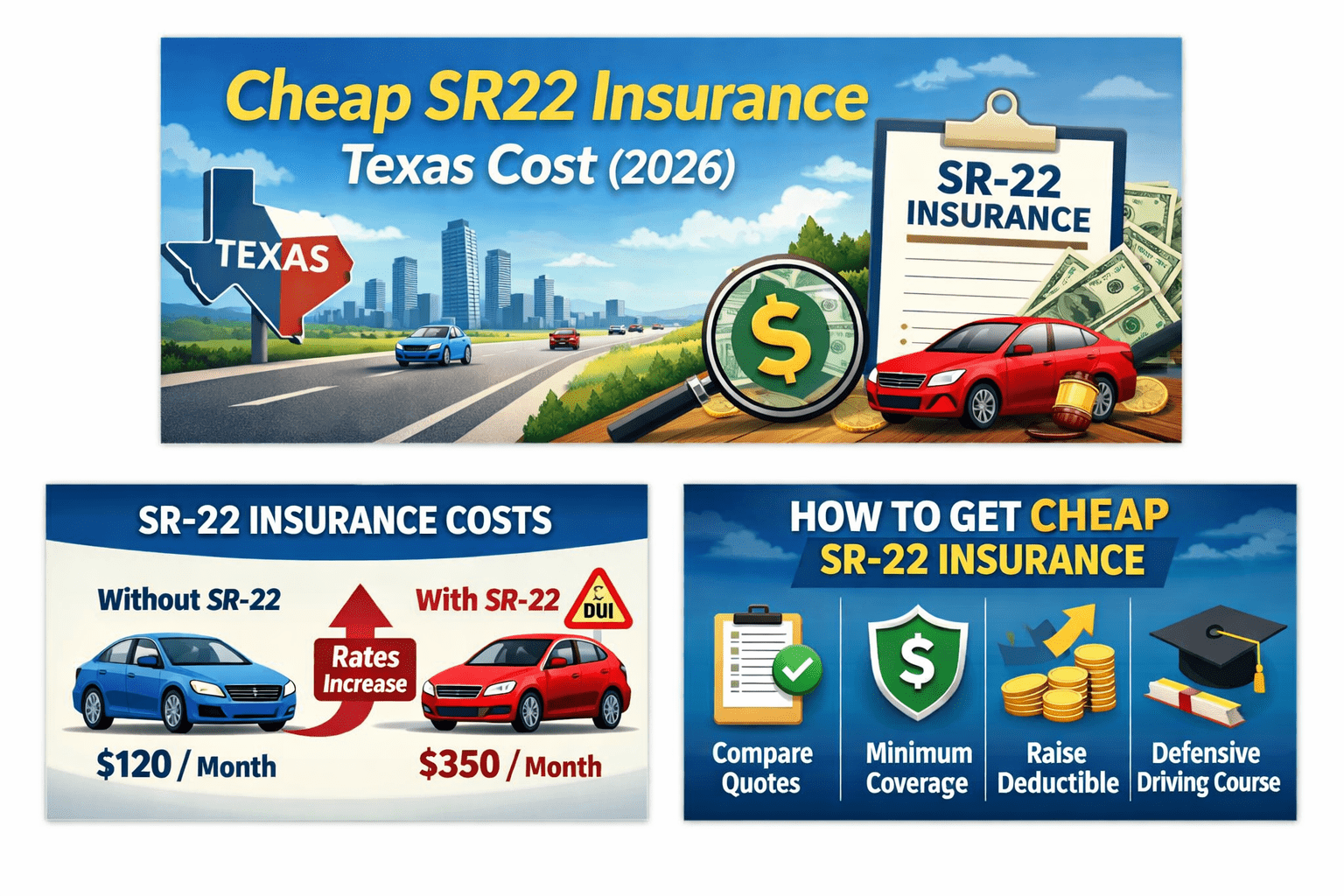

What Does SR-22 Insurance Cost in Texas in 2026?

This is the question everyone wants answered. The honest answer is: it depends. But let’s give you real numbers to work with.

The SR-22 Filing Fee

The SR-22 filing itself is relatively cheap. Most insurers charge between $15 and $50 as a one-time or annual processing fee to file the certificate with the state. That part is not the expensive piece.

The Insurance Premium Increase

The real cost comes from what the SR-22 requirement does to your insurance premium. Because insurers now classify you as a high-risk driver, your rates go up — sometimes dramatically.

Here’s a general breakdown of average annual costs for minimum liability coverage in Texas with an SR-22 in 2026, based on common offense types:

| Offense | Average Annual Premium (Minimum Coverage) |

| No prior insurance | $850 – $1,200 |

| Single DWI/DUI | $1,400 – $2,200 |

| Reckless driving | $1,100 – $1,800 |

| License suspension | $900 – $1,400 |

| Multiple violations | $1,200 – $2,000 |

These figures are for minimum liability coverage only — the legally required baseline in Texas. If you need full coverage (which your lender may require if you have a financed vehicle), the annual premium can climb to $2,500 – $4,500 or more, depending on your record and the vehicle.

For reference, the average Texas driver without violations or an SR-22 requirement pays somewhere between $500 and $700 annually for minimum liability coverage. So yes, the increase is real. But it’s manageable, especially if you shop around.

Cheapest SR-22 Insurance Companies in Texas (2026)

Not all insurers treat SR-22 drivers the same way. Some companies specialize in non-standard or high-risk auto insurance and offer meaningfully lower rates than the big national carriers.

Here are some of the most competitive options for SR-22 drivers in Texas in 2026:

State Farm

State Farm remains one of the more affordable options for SR-22 drivers in Texas, largely because of its size and willingness to insure a broad range of risk profiles. Annual premiums for SR-22 drivers on minimum coverage typically fall in the $900 – $1,300 range, depending on the offense.

Progressive

Progressive is well-known for working with high-risk drivers, and its Snapshot program can actually help bring rates down over time if you demonstrate safe driving habits. Expect to pay somewhere in the $1,000 – $1,500 range for minimum coverage with an SR-22.

Dairyland Insurance

Dairyland is one of the more specialized names in high-risk auto insurance. They cater specifically to drivers who’ve had trouble getting coverage elsewhere, and their rates for SR-22 policies in Texas are often competitive — particularly for drivers with DWI offenses on their record.

The General

The General has built its brand around non-standard auto insurance. Rates tend to be accessible for drivers with serious violations, though you should compare carefully because premiums and coverage terms vary quite a bit.

GEICO

GEICO doesn’t always come up in conversations about SR-22 insurance, but they do file SR-22 certificates in Texas and can be quite competitive for drivers whose only issue was driving without insurance rather than a major moving violation.

Acceptance Insurance

Acceptance Insurance focuses heavily on the non-standard market and operates physical locations across Texas, which is useful if you prefer working with an agent face-to-face rather than entirely online.

The bottom line: get quotes from at least three to five companies before committing to anything. Rates vary significantly depending on your specific offense, your ZIP code, your vehicle, and your age. A quote that takes ten minutes could save you hundreds of dollars over the course of a year.

For a broader look at where SR-22 coverage fits within the overall Texas market, our roundup of the most affordable car insurance in Texas is a solid place to compare your options. [Internal link: Top 5 Most Affordable Car Insurance In Texas]

Non-Owner SR-22 Insurance in Texas

Here’s a situation that trips a lot of people up. What if you need an SR-22 but you don’t own a vehicle?

Maybe you sold your car after a DWI, or you never owned one in the first place but still need your license reinstated. In that case, you need what’s called a non-owner SR-22 policy.

A non-owner policy provides liability coverage when you drive vehicles you don’t own — borrowed cars, rentals, or vehicles belonging to friends or family. It satisfies the state’s SR-22 filing requirement without requiring you to insure a specific vehicle.

Non-owner SR-22 policies are generally cheaper than standard SR-22 policies. In Texas, you can typically find non-owner SR-22 coverage for $300 – $700 per year depending on the reason for the requirement. State Farm, GEICO, Progressive, and Dairyland all offer non-owner policies with SR-22 filing.

One caveat worth knowing: if you regularly drive a vehicle owned by someone in your household, a non-owner policy typically won’t cover those trips. The insurer will likely require that vehicle to be listed on a standard policy instead.

How to Get SR-22 Insurance in Texas: Step by Step

If you’ve never gone through this process, here’s exactly what to expect.

Step 1: Contact an insurance company. Not every insurer in Texas files SR-22 certificates, so confirm upfront that the company handles them. Most major carriers and all non-standard insurers do.

Step 2: Get a quote. Be honest when you apply. The insurer will pull your driving record anyway, and any discrepancy between what you disclose and what they find can result in your policy being cancelled or voided. Give accurate information about your violations and their dates.

Step 3: Purchase the policy and request the SR-22 filing. Once you buy the policy, your insurer files the SR-22 certificate electronically with the Texas DPS. This usually happens within 24 to 72 hours. You’ll receive a copy for your records.

Step 4: Pay the reinstatement fee if applicable. If your license was suspended, the SR-22 filing alone isn’t enough. You’ll also need to pay the Texas DPS reinstatement fee, which typically runs between $100 and $125. Until that’s paid, your license won’t be reinstated even if the SR-22 is already on file.

Step 5: Maintain continuous coverage. For the full duration of the requirement — usually two years — keep your policy active without any lapses. Set up autopay if that helps. The consequences of a lapse aren’t worth risking.

Does SR-22 Insurance Affect Your Credit Score?

No. Filing an SR-22 and purchasing a high-risk auto insurance policy does not directly affect your credit score. The SR-22 is a motor vehicle record item, not a credit or financial record item.

That said, some insurers use a soft pull of your credit history as part of their rating process in Texas, which can influence the premium you’re quoted. This is true for standard policies as well, not just SR-22 situations.

If your credit score is on the lower side, it’s worth knowing that certain insurers — particularly those focused on non-standard policies — rely less heavily on credit scoring in their pricing models. That’s another reason to get multiple quotes rather than assuming the first offer you receive is the best one.

Tips for Lowering Your SR-22 Insurance Costs in Texas

You have more options than you might think when it comes to managing the cost.

Shop around, then shop again. Rates among insurers vary enormously for high-risk drivers. Don’t assume one quote is representative of what the market will offer you.

Choose minimum coverage if your vehicle is older. If your car is paid off and has a low market value, minimum liability coverage may make more financial sense than paying for full coverage. Run the numbers before defaulting to comprehensive and collision.

Ask about available discounts. Even SR-22 drivers qualify for certain discounts: multi-policy bundling, electronic payment discounts, or safe driver programs that track your behavior via app. Most major carriers have something like this available.

Take a defensive driving course. Texas allows licensed defensive driving courses to potentially offset points on your record, and some insurers also offer a discount to drivers who complete an approved course. It won’t eliminate the SR-22 requirement, but it can chip away at your premium.

Stay incident-free. This sounds obvious, but it’s worth saying clearly. Every additional violation while you’re carrying an SR-22 either resets or extends the damage to your record. Treat the SR-22 period as a clean start — drive carefully, keep your insurance active, and you’ll come out the other side in a much better position.

Reevaluate when the requirement ends. Once your SR-22 requirement expires and your insurer removes the filing, get fresh quotes immediately. Your rate should drop substantially at that point, and you may find that switching carriers makes financial sense.

What Happens When the SR-22 Requirement Is Over?

When your two-year (or three-year) requirement ends, your insurer will remove the SR-22 filing from your policy. You’re no longer classified as a high-risk driver by mandate — though your premium may still reflect your driving history for a few more years depending on the carrier’s lookback period.

In Texas, most insurers look back three to five years when calculating your rate. A DWI from four years ago will affect your premium less than one from last year, but it won’t disappear overnight. Each year of clean driving steadily works in your favor.

Once you’re clear of the SR-22 requirement, make it a priority to shop for new coverage. You’re no longer limited to non-standard insurers, and standard carriers will be competitive for your business again. That’s typically when you’ll see your annual premium come down in a meaningful way.

Common SR-22 Mistakes to Avoid

A few things trip people up consistently, and they’re all avoidable.

Letting the policy lapse. Even one missed payment can result in a lapse notification going to the state. Set up autopay or calendar reminders — whatever it takes.

Assuming the SR-22 disappears automatically. Some insurers remove the filing automatically when the requirement ends; others require you to ask. Confirm the process with your insurer well before your end date approaches.

Buying a policy from an insurer that doesn’t file in Texas. Not every insurer is authorized to file SR-22 certificates in this state. Confirm this before purchasing.

Not notifying your insurer if you move. If you move to a different state during your SR-22 period, the filing requirements may change. Texas uses an SR-22; other states may require an FR-44 or a different equivalent. Your insurer needs to know where you’re currently licensed.

Paying too much because you didn’t compare. This is the most common and most avoidable mistake. High-risk insurance doesn’t mean you have to accept the first number you’re quoted. The gap between the cheapest and most expensive SR-22 policy for the same driver in Texas can easily be $500 – $800 per year.

Final Thoughts

Getting hit with an SR-22 requirement is frustrating, no question about it. But it’s not the end of the road — not even close. Millions of Texas drivers have gone through this process and come out the other side with clean records and normal insurance premiums.

The most important things to remember: maintain your coverage without any gaps, choose a policy you can realistically afford month to month, and compare quotes from multiple insurers before committing. The math is simple — two years of consistent, affordable coverage and careful driving is all it takes to leave this behind you.

Use the SR-22 period as a reset. Drive clean, pay on time, and SR-22 insurance in Texas becomes an obstacle you absolutely can manage.

For more context on how SR-22 requirements connect to Texas’s baseline coverage rules, see our full breakdown of the minimum car insurance requirements in Texas. And if you’re comparing your coverage options more broadly, our guide to the most affordable car insurance in Texas covers where SR-22 policies fit within the bigger picture.